Apparently my excursion from the other day left me laid up a while afterwards, so I’ve been using the time to rest, catch up on current events, and read up about one of my other perennial loves: finance.

I can’t mention it enough: a great many people I’ve encountered over the course of my life have great difficulty doing something as simple as balancing a chequebook. They take on too many bad debts at unrealistic interest rates, they take on financial instruments that built with only the short term in mind, they lose track of where the money goes each payday, or they neglect the purpose of creating and protecting a savings. All of these are pathological and may not at first seem to have that much of an impact, but they cause serious damage and a great deal of strife in the end.

Worse still are those who create an artificial crisis: they catastrophize the state of their being to exclude themselves from scrutiny, or choose to stay anchored to circumstances they could extract themselves from — for example, making proactive renovations or repairs to a home that’s bleeding out money through excessive energy bills each month, instead of putting up with the status quo.

Worst of all are those who underestimate inflation, ignore the reality of compound interest, and fail to plan accordingly.

Let’s begin with a bit of a backgrounder.

Inflation is the annual increase in the price of goods, and also the annual decrease in the value of money. In stable economies it tends to be fairly low, but nevertheless it’s an inevitable function of the sum total of all the increases our society sees in its wages, food costs, housing and real estate, commodity values, and other factors. Financial analysts use these in determining the Consumer Price Indices (CPIs), which represent for our purposes what a typical ‘basket’ of goods would cost, then and now.

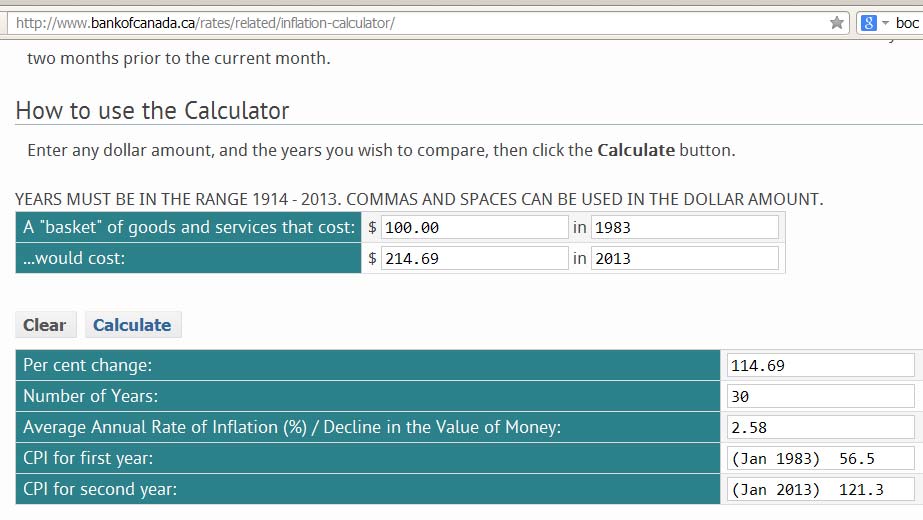

Looking at the last thirty years in Canada:

First, I draw your attention to the averaged yearly inflation rate, 2.58%. While it may be within Bank of Canada targets, this is still very bad news. As you may be aware from comparison shopping across various different financial institutions, almost no one on the market currently offers a savings account with an interest rate above 2%. That means you’re automatically losing money year over year whether you put it in the bank or stick it underneath your mattress.

In the broader scope of things, interest rates in general have gradually been driven down over the course of that same time span, and present-day investments have never looked so sickly. Of course, that’s also because interest rates are being kept artificially low to spur household spending on all manner of goods large and small, be it houses, vehicles, or home computers.

Remember how car loans carried 5.0% to 7.25% base interest all those years ago? Gone! Market forces have not only nixed most essential barriers to entry so that more people can play the game, finance institutions have also made it possible to get quick, cheap gratification through deferred-payment loans systems. You know the type — “Buy now, don’t pay for X number of years.” If you haven’t been living under a rock, you’ve probably noticed these types of schemes are being pushed everywhere … car dealers, furniture stores, electronics retailers, and many more. Instead of saving up and buying when they can afford to buy things, people are steadily taking the bait and living on borrowed funds.

Housing prices have followed a similar pattern: where once the banks expected a reasonable 10% or 20% down payment so the borrower could prove they had the means to stand the test of time on such assets, we as a nation have been gradually lowering the bar. Today you can find intermediaries — or even, heaven forbid, banks — who can assist you in buying a home without any down payment at all! To sweeten the deal, they may also set the deal up on a floating interest rate, which under current conditions means you’ll pay very little interest. Should rates rise in the future, though, and the buyer not be in a position to plan for that contingency, it can get ugly fast.

Credit cards, once a rare phenomenon several decades ago, have also moved in to take up the slack where opportunity knocks but cash flow lacks. They have also come into place in many payment systems as the de facto exchange method because of their convenience, fast authentication technology, and relatively user-friendly interface (eBay is one such example). As testament to both sides of the credit card equation, the average consumer today carries three active credit cards at any given time.

Unfortunately, the credit card system also has a prolific dark side and a tendency toward abuse that has become especially prevalent in recent years. Too many people use it willy-nilly as ‘free money’ instead of as a means to properly mobilize funds they already have in their possession. As a result, the average consumer credit card debt load remains in excess of $3,000, and some never manage to fully pay those balances off.

When you consider that average real wages over the last thirty years have either largely remained stagnant or gone into decline, a fact echoed even by high ranking economists, this shouldn’t really come as a surprise.

Last but not least, there’s the archetypal rite of passage for my generation: the government sponsored student loan. Where once they carried stricter barriers to entry, were more difficult to secure, and originally didn’t tend to doom the borrower to protracted bouts of Ramen noodles and litigation, the landscape has changed dramatically even in just the last decade. The current national average states most undergraduate students end up carrying $19K of debt upon graduation, and that’s just the middle of the range. For those who didn’t take on employment to offset their costs, or for those that failed to plan ahead and seek market insight on the value of their degree, it winds up being the ultimate rude awakening. It is also a literal minefield for anyone who thinks they can discharge these types of loans through bankruptcy — it’s nearly impossible to accomplish, and most times also becomes a magnet for the scorn of sitting court judges. The government wants to see its borrowers make good on their commitments.

All in all, this game of playing fast and loose with financial standards, with everyone seemingly in a race to the bottom as we eliminate sensible protections and barriers to entry, is one that’s become increasingly self-destructive, with fewer people putting aside any meaningful amount of savings, and more people eager to leap into cheap gratification on the things they want.

As a nation we can ill afford to sustain the current systems in place, much less recover in a timely fashion from the burdens our current habits will pose to future generations.

It’s time we gave ourselves a collective reality check.

Remember the part where I quoted the Bank of Canada’s percent change in the cost of goods over the last thirty years? That’s a 114.69% increase. The most revealing part is when you stack that up against the fact that for most, wages have remained stagnant … suddenly, the whole mess begins to make a lot of sense, and it dawns on us why we’re seeing an epidemic of credit card debt, payment delays, high service costs, and exploding household debt loads.

The financial story of our nation has become a strange duality, one of either living above one’s means by dint of the artificial currency solutions our markets offer as a coping mechanism for a cash-strapped society (read: go into debt), or simply cut out what goods and services one can afford to lose without sacrificing the standard of living too severely.

If you must know, I’m from the old school of thought when it comes to such matters: if you can’t afford it, don’t waste time striving for what you cannot have. Do without, and find ways forward. Otherwise, if you must have it, then at least find a way to make it work for you without becoming indebted to someone else.

In other words, don’t be afraid to improvise and especially don’t be afraid to learn along the way or think on your feet — it’s a time where true creative spirit shows its greatest returns.

On this last point, I must also point out that certain projects I’ve completed, particularly the Prometheus Cargo Trailer System, were born out of that exact necessity to find a solution for a practical problem. In my case, I can’t afford a vehicle and don’t drive, so the options for alternate transportation of heavy goods are limited on the commercial front. There are times where one has to move an item between two places and it’s not practical to take a taxi, rent a truck, or else it’s simply more economical to save the money for something else. To fill that gap, I created a bicycle mounted trailer that can move loads in excess of a hundred kilograms — including appliances and certain types of smaller household furniture.

I’d also like to point out that taking on projects like these is representative of a larger do-it-yourself ethos that too many of us have forgotten in a world filled with easily accessible convenience. And, as before, there are times when it simply makes good sense to eschew a little of that convenience, take risks, and put some serious effort into budget choices that will allow us to have those lost dollars and cents trickle back into our pockets, little by little.

You see, while this article isn’t a hard and fast set of rules on budgeting, it does very accurately represent my views, guidelines, and ethics on dealing with finances in the sense that one must be willing to constantly question what’s going on around them, question the status quo, seek out opportunities to apply initiative and creativity, and make that extra little effort to take back what would otherwise bleed away in small amounts each and every month.